Table Of Content

Let’s look at how income plays a role in determining how much you need to buy a house and finding the right home for you. Before you start looking at real estate and shopping around for the right lender, it’s important to take these steps to improve your chances of becoming a homeowner without breaking the bank. Our experts have been helping you master your money for over four decades.

Title Insurance

Keep in mind that the cost of homeownership involves much more than paying the principal and interest on your mortgage loan. You’ll need to also pay homeowners insurance and property taxes, both of which can vary wildly depending on where you’re located. That means general upkeep of the property, as well as repairs as needed. And if your home is part of a homeowners association, there will be HOA fees to pay as well.

Pay Off Debt

Before approving your mortgage, the lender must confirm that your income could support a mortgage payment. For this reason, most lenders need to see 24 months of consecutive employment before you apply for a home loan. The good news is, requirements to buy a house are more lenient than many first-time home buyers expect. Lenders can often be flexible when it comes to things like credit and down payment.

Here's how much money you must make to afford a house in Charlotte, according to Zillow - WCNC.com

Here's how much money you must make to afford a house in Charlotte, according to Zillow.

Posted: Wed, 13 Mar 2024 07:00:00 GMT [source]

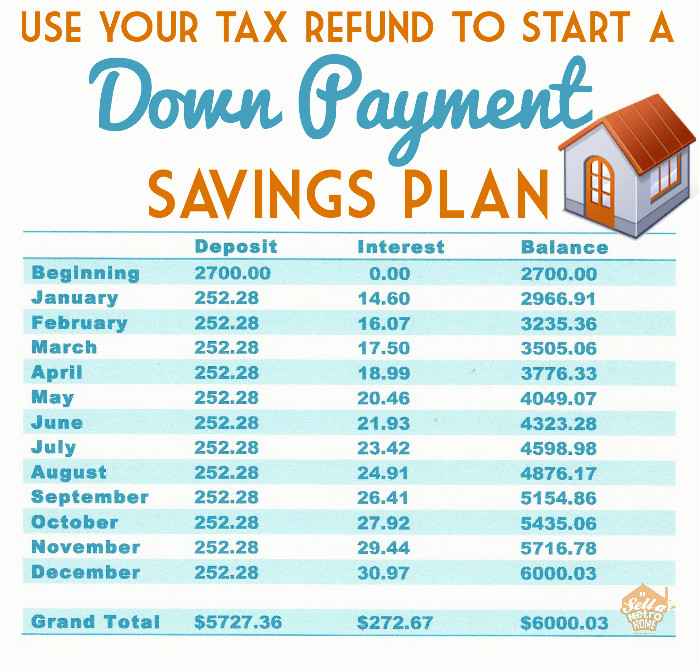

Is $20,000 enough for a down payment on a house?

Building your budget is one of the most important steps in home buying. When buying a home, you sometimes must prepay certain expenses such as property taxes, homeowners insurance or mortgage interest. Your mortgage lender will likely have you make an initial escrow deposit that they’ll put into an account for you. Your lender will then use the escrow account to pay any property taxes, interest or insurance premiums when they come due. Your mortgage rate has a big impact on your monthly mortgage payment, which makes it crucial to shop with multiple lenders for the best mortgage rate.

Mortgage lending guidelines define one month’s reserves as one month’s housing expenses. The calculation includes real estate taxes, association or co-op dues, and property, flood and mortgage insurance premiums, along with principal and interest. Aim for two to six months of all your expenses, not just housing expenses, to give yourself more breathing room. Down payment & closing costsNerdWallet's ratings are determined by our editorial team. The scoring formula takes into account the type of card being reviewed (such as cash back, travel or balance transfer) and the card's rates, fees, rewards and other features.

Ongoing homeownership costs

The amount of money you'll need to purchase a house is highly dependent on the price of the house you plan to purchase. After all, closing costs and down payments are typically represented as a percentage of the home's value. Different lenders have different requirements about how many months’ payments you’ll need in your account. Most lenders require at least two months of cash reserves if you are applying for a conforming mortgage loan. However, the requirement can be as much as 24 months for higher-priced homes. Closing costs will vary depending on the size of your loan, whether a lawyer is present at the closing table, and the fees that your municipality or state charges.

How Much Is A Down Payment On A House? - Bankrate.com

How Much Is A Down Payment On A House?.

Posted: Tue, 09 Apr 2024 07:00:00 GMT [source]

Ideally, the mortgage payment on your new home shouldn’t exceed 28% to 31% of your gross monthly income. Lenders will also look at your debt-to-income ratio, or DTI, to get a clear picture of how risky it is to loan you money. Simply put, the higher your debt-to-income ratio, the more the lender will doubt your ability to pay the loan back. Lenders have maximum DTIs in place that could stand in the way of getting approved for a mortgage.

Credit Score

But a good rule of thumb is to avoid spending more than 28% of your gross income on your monthly mortgage payment. Based on this percentage of income, you can determine the home price you can afford, and ultimately how much cash you’ll need to buy a house. Also referred to as the front-end ratio, this percentage represents the amount of your monthly income that goes towards housing expenses like your mortgage payment, insurance and taxes. In general, experts recommend spending no more than 28% of your income on housing.

Mortgage payment calculator

Closing costs can vary by loan size, loan type, location, or by mortgage lender and can range from less than one percent to higher than six percent. Once you can meet the requirements to buy a house, it’s time to start your home-buying process. First, decide on a real estate agent or Realtor who will help you put an offer on your dream home. If it’s accepted, you’ll schedule a home inspection, get mortgage approved, and do a final walk-through before getting the keys to your new home. Some home buyers make the mistake of house hunting before meeting with a lender. But with a preapproval, you’ll know what homes you can afford before starting the process.

Prices vary based on the size of your home, the distance you’re moving, the weight of your items and whether you’ll need storage for a time in-between. According to HomeAdvisor, a typical move ranges between $913 and $2,528, with the average being about $1,711. Ultimately, figuring out your down payment means thinking about the rest of your budget. You shouldn’t spend every penny you have to cover your down payment — you’ll stretch yourself too thin and stress yourself out as you try to cover all your other necessary expenses.

The content created by our editorial staff is objective, factual, and not influenced by our advertisers. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. When you're deciding whether you're financially ready to buy a house, it's important to account for both the upfront costs of homebuying and the expenses you'll need to budget for after closing.